National Pension System (NPS)

Secure Your Retirement

What Is the National Pension System (NPS)?

National Pension System (NPS) is an investment cum pension plan launched by the Indian Government. This scheme is regulated and administered by the Pension Fund Regulatory and Development Authority(PFRDA). It is specifically launched by the Government of India to offer financial security to Indian senior citizens. NPS scheme provides impressive long-term savings options so that an individual can plan his/her retirement time efficiently by investing in this safe market-based plan.

Top Benefits of NPS

- Long-Term Wealth Growth : With disciplined contributions and market exposure, NPS offers superior long-term returns compared to traditional saving schemes.

- Tax-Efficient Savings : Multiple tax deductions help enhance your net returns

- Expert Fund Management: Your investments are managed by approved PFMs with full transparency.

- Portability & Flexibility: Continue your NPS contributions even if you change jobs or locations.

Types of NPS Accounts

Contribute Regular

Invest in Tier 1 and Tire 2

")

Choose your funds

Select your Investment max

Get Pension Benefits

Enjoy & Steady Retirnment income

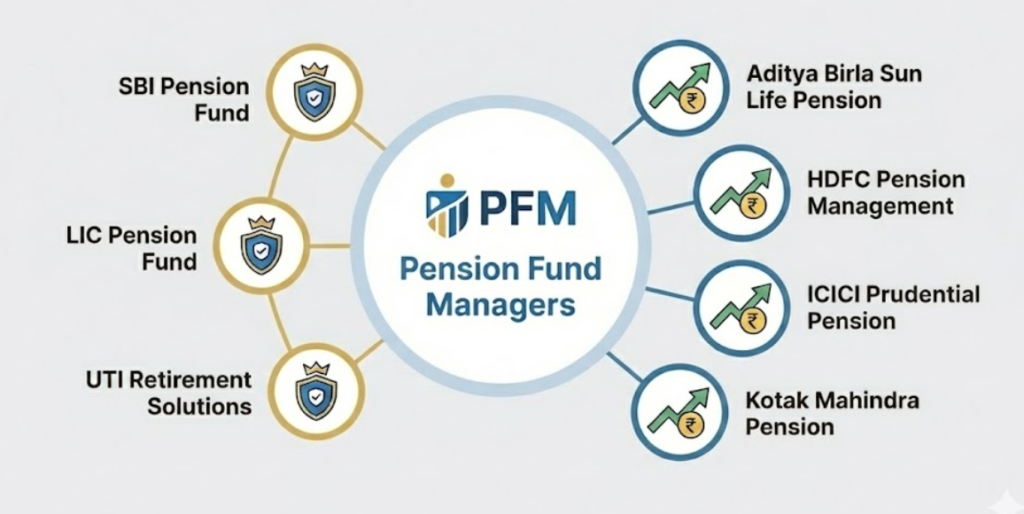

Who are PFMs?

At present, there are seven Pension Fund Managers in the country: Aditya Birla Sun Life Pension Management Limited. HDFC Pension Management Company Limited. UTI Retirement Solutions Limited. SBI Pension Funds Private Limited. ICICI Prudential Pension Funds Management Company Limited. Kotak Mahindra Pension Fund Limited. LIC Pension Fund. SBI Pension Fund, LIC Pension Fund, and UTI Retirement Solutions are the only fund managers who manage pension contributions of government employees under NPS.

What is a PRAN?

PRAN (Permanent Retirement Account Number) is the unique and portable number provided to each subscriber under NPS and remains the same throughout. On successful registration, a PRAN will be allotted to the subscriber. It is a 12 digit number.

Who can join NPS?

Any citizen of India, whether resident or non-resident can join NPS, subject to the following conditions: a) Individuals who are aged between 18-70 years as on the date of submission of his/her application to the POP/POP-SP. b)The citizens either as individuals or as employee-employer groups corporates subject to submission of all required information and Know your customer(KYC) documentation.

Why Choose NPS with Novasure?

Strong Retirement Security

Tax Saving

Market-Linked Growth

Flexible Investment

- Equity (E)

Equity market instruments

- Government Securities

Central & State government bonds

- Corporate Bonds

Corporate debt securities

- Alternate Investment Funds

REITs, InvITs, AIFs (limited exposure)

- Active Choice

Investors decide how their money is allocated across asset classes (E, C, G, A) based on risk appetite and goals.

- Auto Choice (Life Cycle Funds)

Aggressive (LC75) – Higher equity exposure

Moderate (LC50) – Balanced allocation

Conservative (LC25) – Lower equity exposure

- Open Your NPS Account

Fill out a simple application with Novasure.

- Choose Your Investment Strategy

Pick Active or Auto choice based on your goals.

- Start Contributing

Set regular contributions that fit your financial plan.

- Monitor & Adjust

Track your NPS performance and adjust allocations as needed.

Who Should Invest in NPS?

- Young professionals planning for retirement

- Self-employed individuals seeking disciplined long-term savings

- Salaried employees wanting additional tax relief and wealth growth

- Anyone focused on building a secure financial future